As a real estate investor, you're constantly analyzing numbers. But one metric cuts through the noise like no other: the capitalization rate, or cap rate for apartments. It's a quick health check for a building, showing its potential annual return before financing.

For anyone investing in the Monterey Bay area, from Salinas to Carmel, a solid grip on this concept is non-negotiable. According to recent data, national multifamily cap rates climbed to approximately 5.2% by 2024, a significant jump from prior years (Source: CBRE). Understanding why this happens is key to making confident, profitable decisions in our local market.

Decoding the Cap Rate for Apartments

The cap rate is a fundamental tool in any real estate investor's arsenal. At its core, it’s a simple ratio that helps you quickly compare the potential profitability of different properties.

Imagine you're looking at two apartment buildings in Monterey County. One is in a high-demand area of Carmel, and the other is a larger complex in Salinas. The cap rate is your answer for an apples-to-apples comparison.

By expressing a property's income as a percentage of its value, the cap rate helps you evaluate its performance relative to other investment opportunities. It strips away financing complexities to reveal the raw income-generating potential of the asset itself.

This metric is tied directly to both risk and return. A property with a lower cap rate is often seen as a safer, more stable investment. On the flip side, a higher cap rate might offer greater potential returns but could also come with increased risk.

Why This Metric Is Essential for Monterey Bay Investors

Understanding the cap rate for apartments is critical for navigating the unique dynamics of our local market. With our local expertise, we help investors:

- Benchmark Properties: Quickly see if a property's asking price aligns with its income potential compared to similar local buildings.

- Identify Opportunities: Spot undervalued assets where you can boost income and, in turn, raise the property's value.

- Gauge Market Trends: Track how cap rates are changing in Monterey, Salinas, and Carmel to understand broader shifts in investor sentiment.

Economic conditions have a huge influence on these rates. For instance, national apartment cap rates moved from around 4.1% in 2021 to approximately 5.2% by 2024, largely due to interest rate hikes. This shows just how directly larger financial trends impact local properties. You can explore more about these multi-family market trends and their drivers in recent years.

Ultimately, mastering the cap rate allows you to move beyond gut feelings and start making data-driven decisions. It's the first step toward building a successful real estate portfolio here on the beautiful Central Coast.

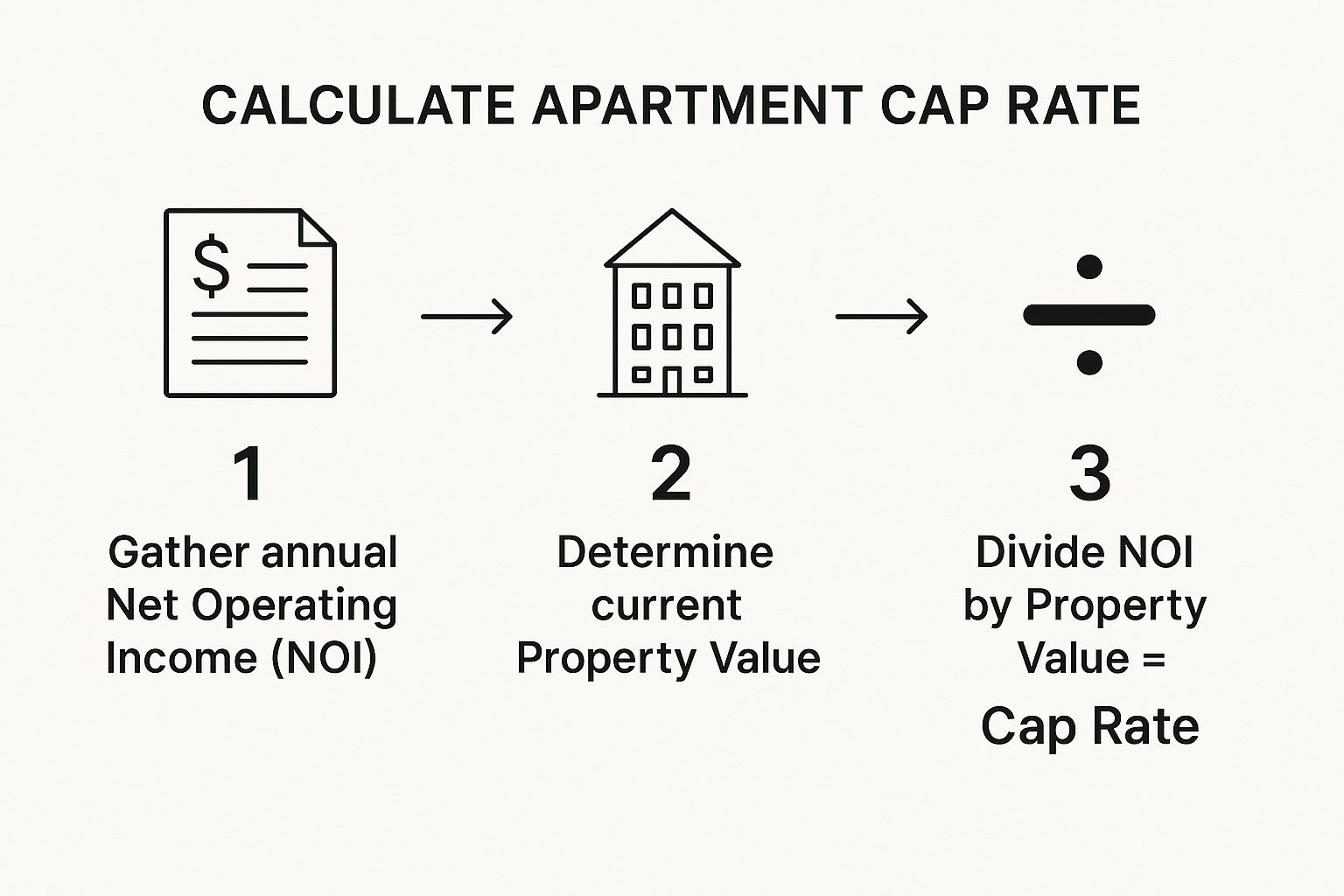

How to Accurately Calculate Cap Rate

Let's walk through the cap rate formula step-by-step. The formula itself is straightforward, but the real skill lies in getting the inputs right. Nailing this calculation is the foundation for any solid analysis of a potential apartment investment.

The core equation is simple: Cap Rate = Net Operating Income (NOI) / Current Market Value. Think of NOI as the property's annual profit before you factor in your mortgage or income taxes. Getting this number right is the most critical part of the process.

This visual guide breaks down the simple, three-step process for figuring out the cap rate for apartments.

As you can see, the calculation flows logically from gathering your income and expense data to determining the property's value, which finally reveals the cap rate.

Step 1: Start with Gross Potential Income

First, you need to figure out the property's total potential income for a full year. This includes every single dollar the property could possibly generate.

Your calculation should include:

- Gross Rental Income: This is what you’d collect if every unit was occupied 100% of the time at its full market rate.

- Other Income Sources: Don’t forget about extra revenue streams like laundry machines, assigned parking, storage units, or pet fees.

This number represents your best-case scenario and is the starting point for painting a more realistic financial picture.

Step 2: Calculate Net Operating Income

Now, it's time to find your Net Operating Income (NOI). To do this, you'll subtract all necessary operating expenses from your gross income.

It’s absolutely essential to be thorough here. Operating expenses are all the costs required to run and maintain the building day in and day out.

Key Takeaway: NOI is the true measure of an apartment building's profitability from its operations. It purposely excludes financing costs (like mortgage payments) and capital expenditures (major one-off replacements like a new roof).

Common operating expenses to subtract include:

- Property Management Fees

- Property Taxes

- Insurance Premiums

- Utilities (if not paid by tenants)

- Routine Repairs and Maintenance

- Vacancy Loss (a realistic estimate for unoccupied units)

Tracking these expenses meticulously is non-negotiable. To make this process seamless, many landlords find the best accounting software for landlords invaluable for keeping their financial records clean.

To see this in action, let's look at a hypothetical 10-unit apartment building in Monterey.

Sample NOI Calculation for a Monterey Apartment Complex

| Income/Expense Item | Annual Amount | Notes |

|---|---|---|

| Gross Potential Rent | $240,000 | $2,000/month per unit x 10 units x 12 months |

| Other Income | $3,600 | Laundry, parking, etc. |

| Gross Potential Income | $243,600 | Total possible income |

| Vacancy Loss (5%) | ($12,180) | An industry-standard estimate |

| Effective Gross Income | $231,420 | Income after accounting for vacancy |

| Property Taxes | ($25,000) | Based on assessed value |

| Insurance | ($7,500) | Annual premium |

| Utilities | ($6,000) | Common area electricity, water, trash |

| Repairs & Maintenance | ($12,000) | Budgeted at $100/unit per month |

| Property Management (8%) | ($18,514) | Based on Effective Gross Income |

| Total Operating Expenses | ($69,014) | Sum of all expenses |

| Net Operating Income (NOI) | $162,406 | EGI – Total Operating Expenses |

This breakdown clearly shows how we get from a simple rent roll to a powerful, decision-making number like NOI.

Step 3: Determine the Property Value

The final piece of the puzzle is the property's current market value. This isn't what you paid five years ago; it's the price the property would realistically sell for in today's Monterey Bay market.

You can determine this value in a few ways:

- Using the Asking Price: For a property you're looking to buy, the seller's list price is your starting point.

- Reviewing Comparable Sales: Look at what similar apartment buildings in the same area—like Salinas or Marina—have recently sold for.

- Getting a Professional Appraisal: For the most accurate figure, a commercial real estate appraiser provides a detailed valuation.

Once you have a reliable NOI and a solid market value, you just divide the first by the second. That final percentage is your cap rate, a powerful tool for comparing investment opportunities across our diverse local communities.

What Really Drives Apartment Cap Rates

Ever wonder why one apartment building has a 4% cap rate while another sits at 7%? The answer boils down to two forces: risk and opportunity. A cap rate is the market's way of pricing the perceived risk tied to a property's future income.

Think of it like this: a low cap rate property is like a stable, blue-chip stock—a safe bet with predictable returns. A high cap rate property is more like a growth stock, offering higher potential returns but also more uncertainty.

These perceptions of risk are shaped by economic trends, local market conditions, and the unique DNA of the property itself.

The Big Picture: Macro-Economic Factors

Forces far beyond Monterey Bay have a direct impact on the cap rate for apartments right here. These macro-level factors set the stage for the investment environment.

The most significant driver is interest rates. When borrowing costs go up, investors demand higher returns, which almost always causes cap rates to rise. We saw this play out recently as the Federal Reserve's rate hikes pushed multifamily cap rates up nationally. It's a clear demonstration of how interest rates and multifamily cap rates are connected.

Other key factors include:

- Credit Availability: When lenders tighten their standards, it becomes harder for buyers to get financing, which can lead to higher cap rates.

- Overall Economic Health: A strong national economy with low unemployment often leads to lower, more compressed cap rates.

Local Market Dynamics Matter Most

While national trends set the tone, the real story is always local. Conditions within Monterey County, from Salinas to Carmel, have a huge influence on property-specific cap rates. This is where our deep local expertise becomes your critical advantage.

Local job growth is a primary driver. A thriving local economy, like the agricultural powerhouse in Salinas, creates strong demand for rental housing. That translates to lower vacancy rates and the potential for steady rent growth, leading to more attractive cap rates for investors.

Key Insight: A property's cap rate is a direct reflection of its location's economic strength and desirability. The more stable and in-demand an area is, the lower the perceived risk, and thus, the lower the cap rate.

Factors like population growth, local development, and housing supply all play a crucial role. An area with little new construction but a growing population will naturally command lower cap rates.

Property-Specific Characteristics

Finally, the analysis drills down to the building itself. Two properties on the same block can have wildly different cap rates based on their individual traits.

Important property-level factors include:

- Building Age and Condition: A newly renovated building presents far less immediate risk than an older property with deferred maintenance.

- Tenant Quality and Lease Strength: A building full of stable, long-term tenants is much less risky than one with high turnover.

- Location Desirability: Is the property near major employers or good schools? A prime location within Monterey significantly lowers risk and the cap rate.

- Potential for Improvement: An investor might accept a higher initial cap rate if they see a clear path to increasing the NOI through smart renovations or better management.

For out-of-town investors, having a trusted, bilingual partner on the ground to assess these factors is essential. Professional oversight ensures the on-paper numbers align with reality, a core part of our approach to rental property management for out-of-town owners.

Finding a Good Cap Rate in Monterey Bay

Trying to define a single “good” cap rate for apartments is impossible. A number that looks amazing in one neighborhood could be a massive red flag just a few miles away. The real question is, "what's a good cap rate for this specific area and this type of building?"

This is where true local expertise becomes an investor's most powerful tool. The Monterey Bay region isn't one uniform market; it’s a mosaic of unique sub-markets.

The Trade-Off Between Carmel and Salinas

Let's walk through a real-world scenario. You might see an apartment building in a prime Carmel location listed with a 4.5% cap rate. At the same time, a similar property in Salinas is advertised at 6.5%.

On paper, the Salinas property looks like the clear winner. But when you look closer, you see a classic investment trade-off playing out.

A lower cap rate often signals a higher-quality asset in a more stable, desirable location. Investors are willing to pay a premium—and accept a lower initial yield—for the perceived safety and long-term appreciation potential that areas like Carmel or Pacific Grove offer.

The 4.5% cap rate in Carmel tells a story of high tenant demand and strong appreciation potential. The 6.5% cap rate in Salinas offers better immediate cash flow but might reflect higher perceived risks. Neither is inherently "bad"—they are simply different investment types that align with different goals.

Looking Beyond the Listing Sheet

Never forget that the cap rate on a listing is just a starting point. It's an advertisement, often calculated with rosy numbers that might not hold up in the real world. You find the true value by digging deeper into what actually drives a property's Net Operating Income (NOI).

This is where a hands-on, local perspective becomes non-negotiable. Knowing that a specific Salinas neighborhood is slated for redevelopment, for example, could completely change your forecast for rent growth. These are the details you'll never find on a spreadsheet. For more on this, check out our property management tips built for Monterey Bay investors.

Local Expertise Is Your Greatest Asset

At the end of the day, finding a good cap rate in Monterey Bay is about understanding the story behind the number. It demands an intimate knowledge of each community's economic pulse and rental demand.

An investor armed with this insight can confidently decide if a cap rate signals a premium asset or a value-add opportunity. Without that local context from a trusted partner, you're just guessing.

Common Mistakes Investors Make with Cap Rates

The cap rate is a fantastic tool, but treating it as the final word is a trap that trips up even experienced investors. Using this metric in a vacuum can be incredibly misleading.

One of the biggest mistakes is blindly trusting a seller's pro-forma numbers. These figures often paint a perfect picture with 100% occupancy and suspiciously low expenses. A smart investor always creates their own underwriting based on realistic, verifiable data.

Ignoring Hidden Costs and Deferred Maintenance

A juicy high cap rate might be hiding serious problems. Deferred maintenance is the classic example. A leaky roof or an old HVAC system won't show up in current expenses, but they will absolutely wreck your future Net Operating Income (NOI).

These looming capital expenditures can vaporize any gains you thought you were getting. This is why you must conduct a thorough property inspection to uncover these hidden costs.

Key Insight: A cap rate is only as reliable as the NOI used to calculate it. If the income is inflated or the expenses are understated, the resulting cap rate is fundamentally flawed and will lead to poor investment decisions.

If you don't budget for inevitable increases in taxes and insurance, your actual cash flow will fall far short of your projections.

Making Flawed Apples-to-Oranges Comparisons

Comparing cap rates without context is another huge pitfall. A 4% cap rate on a Class A building in Monterey represents a completely different risk profile than a 7% cap rate on a Class C building elsewhere.

Market dynamics can also shift quickly. Since early 2022, rising interest rates have pushed U.S. multifamily apartment cap rates up significantly, causing a slowdown in deals. You can read more about these recent multifamily cap rate shifts to see the full impact.

Overlooking Management and Local Nuances

Finally, many investors underestimate how much management impacts the bottom line. Inefficient management can lead to higher vacancies and out-of-control expenses—all things that directly hurt your NOI. This is especially true for out-of-town investors, like military families who need someone reliable watching over their property. We dive into this in our guide to rental management for deployed military personnel.

At Torrente Property Management, our integrity and responsiveness ensure your asset is protected. The cap rate is just a starting point; we provide the deep analysis that follows.

Time to Put Your Knowledge to Work

Let's bring this all together. The cap rate for apartments is a fantastic starting point for sizing up risk and potential return, but you must look at the whole picture. It's a powerful tool, not a magic number.

The road to successful real estate investing in Monterey Bay is paved with informed decisions. This means digging deeper than advertised numbers, understanding local market factors, and sidestepping common mistakes.

Key Takeaways for Your Next Investment

True mastery comes from doing the right things repeatedly. The most successful local investors perform rigorous due diligence. They know a cap rate is only as good as the numbers behind it.

Here are the critical points to remember:

- Always Verify the NOI: Never take a seller's numbers at face value. Build your own projections based on real-world data.

- Context Is King: Understand the specific property type, its exact location, and current market conditions. A 5% cap rate in Pacific Grove tells a different story than a 5% cap rate in Salinas.

- Think Long-Term: Use the cap rate to assess not just today's performance but tomorrow's potential.

Final Takeaway: Your goal isn't just to find a property with a tempting cap rate; it's to find a solid investment where the numbers make sense after you've kicked the tires. Your confidence comes from that disciplined process.

If you're ready to put this knowledge into action, our team is here to give you the local expertise and personalized service you need. We are committed to helping our community thrive, one well-managed property at a time.

For a personalized chat about your investment goals, contact Torrente Property Management today at (831) 582-8916.

FAQs About Apartment Cap Rates

We've put together some straightforward answers to the questions we hear most often about the cap rate for apartments.

Is a higher or lower cap rate better?

Neither is inherently "better"—it depends on your investment strategy. A low cap rate (e.g., 4-5%) usually signals a lower-risk property in a high-demand area, ideal for investors focused on long-term appreciation. A high cap rate (7%+) often means higher immediate cash flow but comes with more risk, suiting investors who prioritize current income.

How do interest rates affect apartment cap rates?

Interest rates and cap rates typically have an inverse relationship. When interest rates rise, borrowing becomes more expensive, so investors demand higher returns (higher cap rates) to make a deal worthwhile. When interest rates fall, financing is cheaper, which increases buyer demand and pushes property values up, causing cap rates to go down.

What is the difference between cap rate and ROI?

The cap rate measures the property's unleveraged return based on its income and market value, making it great for comparing different assets. Return on Investment (ROI), specifically cash-on-cash return, measures the return on your actual cash invested, factoring in your specific financing. Cap rate evaluates the property; ROI evaluates your deal.

Can a cap rate be negative?

Yes, and it’s a massive red flag. A negative cap rate means a property's operating expenses are higher than its gross income, so it is losing money before any mortgage payments are made. This signals a deeply troubled asset that should be avoided unless you have a clear, well-funded turnaround plan.

How can I increase property value using the cap rate formula?

The formula Value = NOI / Cap Rate shows that the most direct way to increase value is by increasing your Net Operating Income (NOI). You can achieve this by boosting revenue (raising rents, adding fees) or cutting expenses (energy-efficient upgrades, renegotiating contracts). Excellent property management also reduces vacancies, stabilizing your NOI and building long-term value. Our guide on tenant selection and screening tips is a fantastic resource for this.