A commercial lease agreement template is a basic form that outlines the rules for a business renting a property. While it's a good starting point, using a generic version from the internet without expert review is a major risk for your business.

Why Your Business Needs a Solid Lease Agreement

Whether you’re a landlord in Salinas or a new tenant in Carmel, a lease is more than a rental contract. It is the legal and financial foundation for your business operations. A weak lease can lead to surprise costs and legal battles later.

The stakes are high. A recent survey showed that over 68% of real estate professionals expect leasing activity to increase (Deloitte). This makes understanding your lease more important than ever for Monterey Bay business owners.

The Dangers of a One-Size-Fits-All Template

Using a generic commercial lease agreement template is like building on a shaky foundation. It might look fine at first but won't hold up under pressure. These templates rarely account for the specific needs of your business or local Monterey Bay area rules.

Here are a few risks:

- Vague Language: Unclear terms about who pays for maintenance or repairs can lead to costly disagreements.

- Unfavorable Clauses: A standard template might lock you into automatic rent hikes or strict rules that limit your business growth.

- Missing Protections: It likely lacks key clauses for tenants, like options to renew the lease or sublease the space if your needs change.

A well-crafted lease is an investment in your business's stability. It provides clarity, protects your rights, and prevents expensive conflicts.

Your Lease Is Your Business Blueprint

Think of your commercial lease as the blueprint for your business's physical location. It defines more than just your rent; it sets the rules for how you operate in the space. For a restaurant in Monterey, this could involve rules about outdoor seating.

A custom agreement ensures your business needs are spelled out and legally protected. It turns a standard document into a tool that supports your long-term goals. Taking time to get it right from the start is one of the smartest moves you can make.

Breaking Down Key Lease Clauses

A commercial lease agreement can be full of confusing legal terms. Whether you're a landlord in Monterey or a tenant in Salinas, understanding these key parts is essential to protect your interests. Let's look at the most important sections in plain English.

Lease Term and Rent Structure

The lease term sets how long the rental agreement will last, typically from three to ten years. The start and end dates must be perfectly clear. For a tenant, a longer term offers stability, while a shorter term gives a landlord more flexibility.

The rent structure is also critical. It’s not just about the amount, but how it might change over time. Common models include:

- Fixed Rent: The rent amount stays the same for the entire term. Simple and predictable.

- Rent Escalations: The rent increases at set times, usually each year, by a fixed percentage or based on an inflation index.

- Percentage Rent: Common in retail, the tenant pays a base rent plus a percentage of their gross sales after reaching a certain target.

Getting these details right helps you plan your finances and negotiate terms that work for your business.

Common Commercial Lease Types Explained

The lease type determines who pays for the property's operating expenses. This is a huge factor in your total cost. Understanding the difference between a Gross Lease and a Triple Net (NNN) lease can prevent major financial surprises.

Here's a simple comparison.

| Lease Type | Who Pays Property Expenses (Taxes, Insurance, Maintenance) | Best For |

|---|---|---|

| Gross Lease / Full-Service Lease | Landlord pays all operating expenses. The tenant pays one flat rate. | Tenants who want predictable, all-inclusive monthly costs. |

| Modified Gross Lease | Shared. The landlord and Tenant split certain operating costs as negotiated. | Those looking for a flexible middle ground between a Gross and NNN lease. |

| Net Lease | Tenant pays base rent plus one or more of the main property expenses. | Landlords who want to pass specific operational costs to the tenant. |

| Double Net Lease (NN) | Tenant pays base rent plus property taxes and insurance. | Investors who prefer fewer management duties but will handle major repairs. |

| Triple Net Lease (NNN) | Tenant pays base rent plus all three major expenses: property taxes, insurance, and maintenance. | Landlords seeking a passive investment and tenants who want full control. |

It's vital that both parties know exactly what they are agreeing to before signing.

Security Deposits and Maintenance Duties

The security deposit is the landlord's financial safety net. It covers potential property damage or unpaid rent. California's rules for commercial deposits are more flexible than for residential ones, so the lease must clearly state the amount and conditions for its return.

Maintenance is another common issue. Who pays when the HVAC system breaks? The lease must assign these duties clearly to avoid expensive disputes. This clarity is just as important as what you'd find in a detailed property management contract.

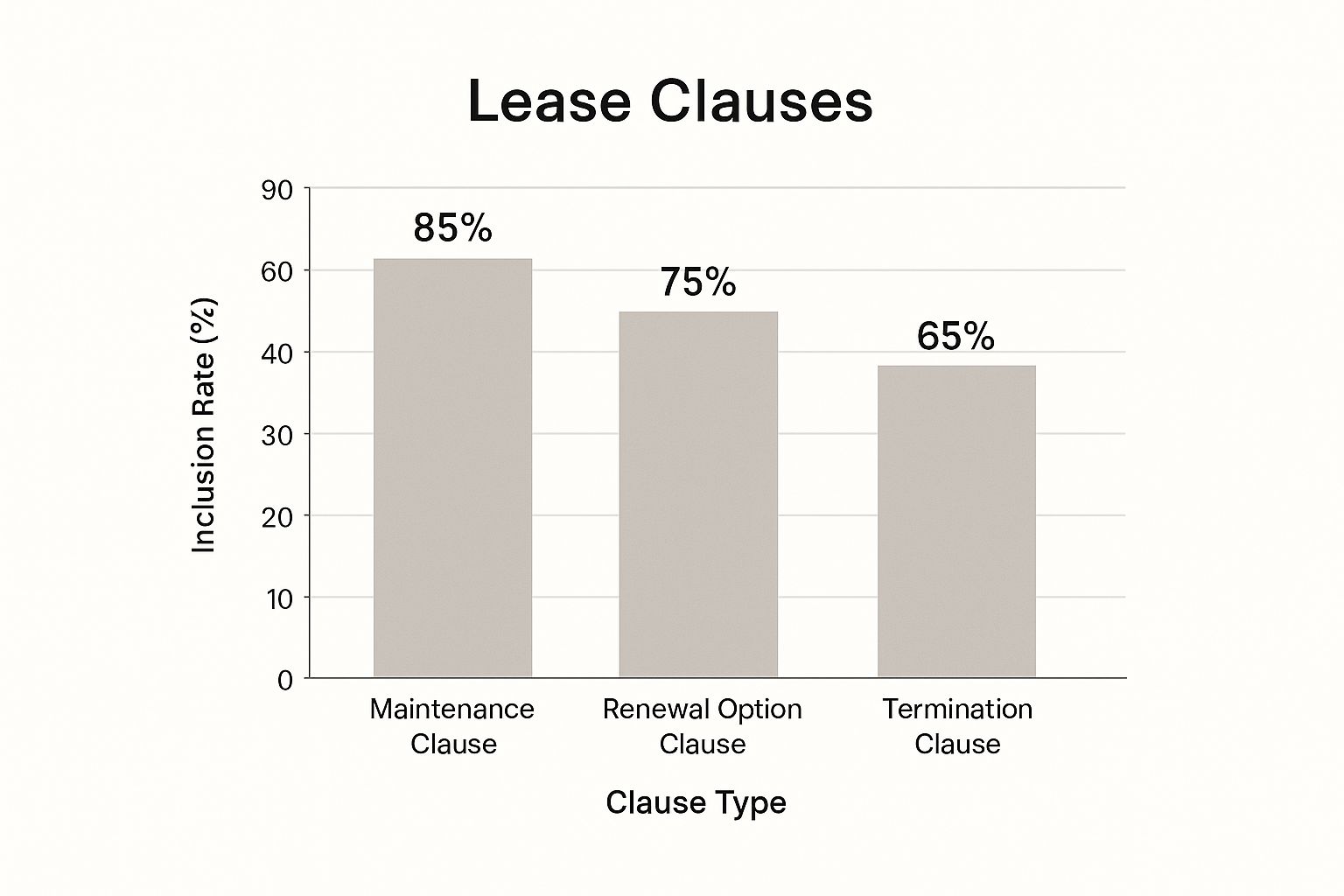

The infographic below shows how common these clauses are.

As you can see, maintenance clauses are standard. However, renewal options and termination rights are less common and often require negotiation.

Permitted Use and Exclusivity

For a tenant, the "permitted use" clause is critical. It defines what kind of business activities you can conduct on the property. A vague phrase like "general retail use" could be a problem for a specialized business, like a Carmel art gallery needing to host events.

Pro Tip: Tenants should seek the broadest use clause possible for future flexibility. Landlords usually prefer a narrow definition to control the tenant mix.

An exclusivity clause is a powerful tool for tenants in a multi-tenant property. It prevents the landlord from renting another space to a direct competitor. This can give your business a major advantage and is worth negotiating for.

Tailoring Your Lease for the Monterey Bay Market

A generic commercial lease from the internet is not enough for the Monterey Bay area. Our local market is unique. A one-size-fits-all document will miss key details for a business in tourist-heavy Carmel or the agricultural hub of Salinas.

Adapting a template isn't just a good idea—it's essential for protecting your investment. The needs of a shop on Alvarado Street in Monterey are very different from a warehouse near the Salinas airport. You must adjust the terms to fit these local realities.

Addressing Local Zoning and Business Needs

Every city here, from Pacific Grove to Soledad, has its own zoning laws and business rules. These local regulations affect everything from signs to operating hours. A standard template will not account for these important details.

For example, a restaurant lease in Carmel-by-the-Sea must follow strict historic preservation codes. Meanwhile, a business in the Salinas Valley might need specific clauses for agricultural land use or seasonal operations.

When you customize your commercial lease for the local market, you create a strategic tool. It keeps you compliant and aligns the contract with the economy of Monterey County.

Crafting Clauses for a Seasonal Economy

Many businesses around Monterey Bay depend on a seasonal economy. This is especially true in tourist spots like Cannery Row. A business might earn 70% of its revenue in the summer, making a fixed-rent lease difficult in the slow months.

Here's how to build in flexibility:

- Variable Rent Structures: You could negotiate a lower base rent during the off-season, balanced with a higher rent when business is busy.

- Temporary Use Permits: Your lease should explain how to get permits for seasonal events or sidewalk sales common in our coastal towns.

- Co-Tenancy Clauses: This clause can offer rent relief if a major anchor store that drives foot traffic leaves, protecting your business.

These details are vital, especially for landlords who don't live here and may not understand local market cycles. Managing these issues is a key part of our rental property management for out-of-town owners.

How to Negotiate Your Lease with Confidence

Your commercial lease agreement template is just the starting point. Almost every term is negotiable. A successful negotiation turns a standard document into a balanced agreement that works for everyone.

The goal is to find a middle ground that protects both parties. For example, a new Monterey restaurant needed major upgrades. Through smart negotiation, the landlord provided a Tenant Improvement Allowance (TIA) to help cover the costs in exchange for a longer lease. It was a win-win.

Focus on Key Negotiation Points

While you can discuss any clause, focus your energy on a few key areas for the best results.

Here are the high-impact items to zero in on:

- Rent Escalations: Don't just accept a fixed annual increase. Propose a cap or tie the increase to the Consumer Price Index (CPI) to protect your budget.

- Renewal Options: As a tenant, securing the option to renew your lease provides stability without a long-term commitment from the start.

- Exit Clauses: Business can be unpredictable. Negotiating an early termination or sublease clause gives you flexibility if your needs change.

A lease negotiation isn't about one side winning. It's about building a partnership that is fair, clear, and sustainable for both parties.

Preparing for a Productive Discussion

Confidence at the negotiating table comes from preparation. Before you talk, know exactly what you want.

Make a list of your "must-haves" and "nice-to-haves." Researching similar properties in Salinas or Carmel also provides powerful leverage. Knowing current market rates and terms helps you make a strong case.

Finally, get everything in writing. Once you agree on a point, make sure it is reflected in the final lease. Before signing, have a clear plan for the end of the lease. Understanding your move-out duties is key, which is why our tenant move-out inspection checklist is so helpful.

Common Lease Mistakes and How to Avoid Them

The biggest risks in a commercial lease are often hidden in legal jargon. A small oversight during signing can become a huge financial problem later. It is important to be proactive to protect your investment.

The most expensive lease is the one you don't fully understand. Let’s look at common pitfalls and how to avoid them.

Overlooking Vague or Ambiguous Language

Vague terms are a dangerous trap. Phrases like "landlord will maintain the property in good condition" sound fine but are legally weak. What does "good condition" actually mean?

Without specific details, you are inviting future arguments. If the HVAC fails, this vague language can lead to a long and costly fight over who pays for the repair.

The solution? Define everything. Insist on clear language for all responsibilities.

- Maintenance: Detail which party is responsible for the roof, plumbing, and HVAC.

- Repairs: Specify timelines for how quickly critical repairs must be made.

- Common Areas: Outline who pays for the upkeep of shared spaces like lobbies and parking lots.

This detail removes guesswork and protects both the tenant and the landlord.

Ignoring Default and Remedy Clauses

Many people skim the "Default" section, but this is a mistake. This clause explains what happens if either party fails to meet their obligations. A poorly written clause might allow a landlord to evict you for a minor issue.

The Default and Remedy clause is a roadmap for resolving conflicts fairly. Ensure it includes reasonable notice periods and chances to "cure" a violation before drastic action is taken.

Neglecting Insurance Requirements

Insurance clauses are often dense and easy to gloss over. Failing to understand these requirements can be a costly error. You might pay for more coverage than you need or find out you're underinsured after an accident.

A common mistake is not checking that your policy meets the specific types and amounts of coverage required in the lease. This puts your business at financial risk. Using the best accounting software for landlords can help track these expenses.

Market conditions can give you leverage to negotiate better terms. Check the National Association of Realtors' latest insights to stay informed.

FAQs: Your Commercial Lease Questions Answered

Diving into a commercial lease agreement brings up many questions. Here are clear answers to common questions we hear from landlords and tenants across the Monterey Bay area. Our goal is to clear up confusion so you can move forward with confidence.

What's the difference between a gross lease and a net lease?

A gross lease is like an all-inclusive deal where the tenant pays one flat rental fee. The landlord handles all other property expenses, like taxes and insurance. This offers tenants predictable monthly costs.

A net lease is different. The tenant pays a lower base rent but also covers some of the property's operating costs. The most common is a Triple Net (NNN) lease, where the tenant pays for taxes, insurance, and maintenance.

Can I break a commercial lease in California?

Breaking a commercial lease is very difficult and usually results in large financial penalties. California law offers few protections for commercial tenants who want to exit a lease early. Always consult a real estate attorney before trying to end your lease ahead of schedule.

What is a Tenant Improvement Allowance (TIA)?

A Tenant Improvement Allowance (TIA) is money a landlord provides to help a tenant customize their new space. It’s a construction budget to help you prepare the property for your business. The TIA amount is negotiated directly into the lease.

Do I need a lawyer to review my lease?

Yes, absolutely. We strongly advise both landlords and tenants to have a real estate attorney review their commercial lease before signing. An attorney can spot unfavorable terms and ensure the agreement protects your legal and financial interests.

How long are typical commercial leases?

Commercial leases are typically much longer than residential ones. A standard term can range from three to ten years. The final length depends on the property, current market conditions, and the needs of both the landlord and the tenant.

A strong, clear lease is the foundation of a successful commercial tenancy. If you have questions about managing your Monterey Bay commercial property, Torrente Property Management is here to help. Our bilingual team offers the local expertise and trustworthy service you need.

Contact Torrente Property Management today at (831) 582-8916 to discuss your needs.